The Diversification Myth - The Facts

Diversification is often seen as a magic shield in investment advice. But in crises, the theory often fails and expensive portfolio complexity eats up returns. We show how real crisis protection works.

Diversification Myth: When Bad Advice Becomes Expensive

In investment advice, there is a dogma that is revered almost religiously: diversification. Since Harry Markowitz founded Modern Portfolio Theory in the 1950s, his statement has been regarded as the ultimate promise: 'Diversification is the only free lunch on the stock market.'

The story told by many financial advisors is as simple as it is tempting: don't put all your eggs in one basket. When stocks fall, bonds, commodities, or gold cushion the losses. A broadly diversified portfolio fluctuates less and protects against ruin. However, behind this 'magic shield' lies a reality that often costs investors dearly. Because due to bad or ill-considered advice, this concept is often not used for protection today, but instead leads to completely overloaded portfolios and unnecessary costs.

The Illusion of Stability

The foundation of classic diversification advice is the assumption that correlations between asset classes are stable. But what exactly is this 'correlation'?

Put simply, it measures how much two things move in lockstep. Imagine a classic seesaw on a playground: if one side goes down, the other automatically goes up. This is called a perfect negative correlation (-1). If two things move completely independently of each other – like the rainy weather in London and the price of a loaf of bread in Zurich – the correlation is zero (0). And if two things do exactly the same thing, like two dancers in a perfect synchronized dance, they have a correlation of +1.

The goal of classic investment advice is to mix assets into your portfolio that, in the best case, sit on the seesaw or at least dance completely independently of each other. When stock prices fall, another asset (such as bonds or gold) should rise or at least remain stable to cushion the overall loss.

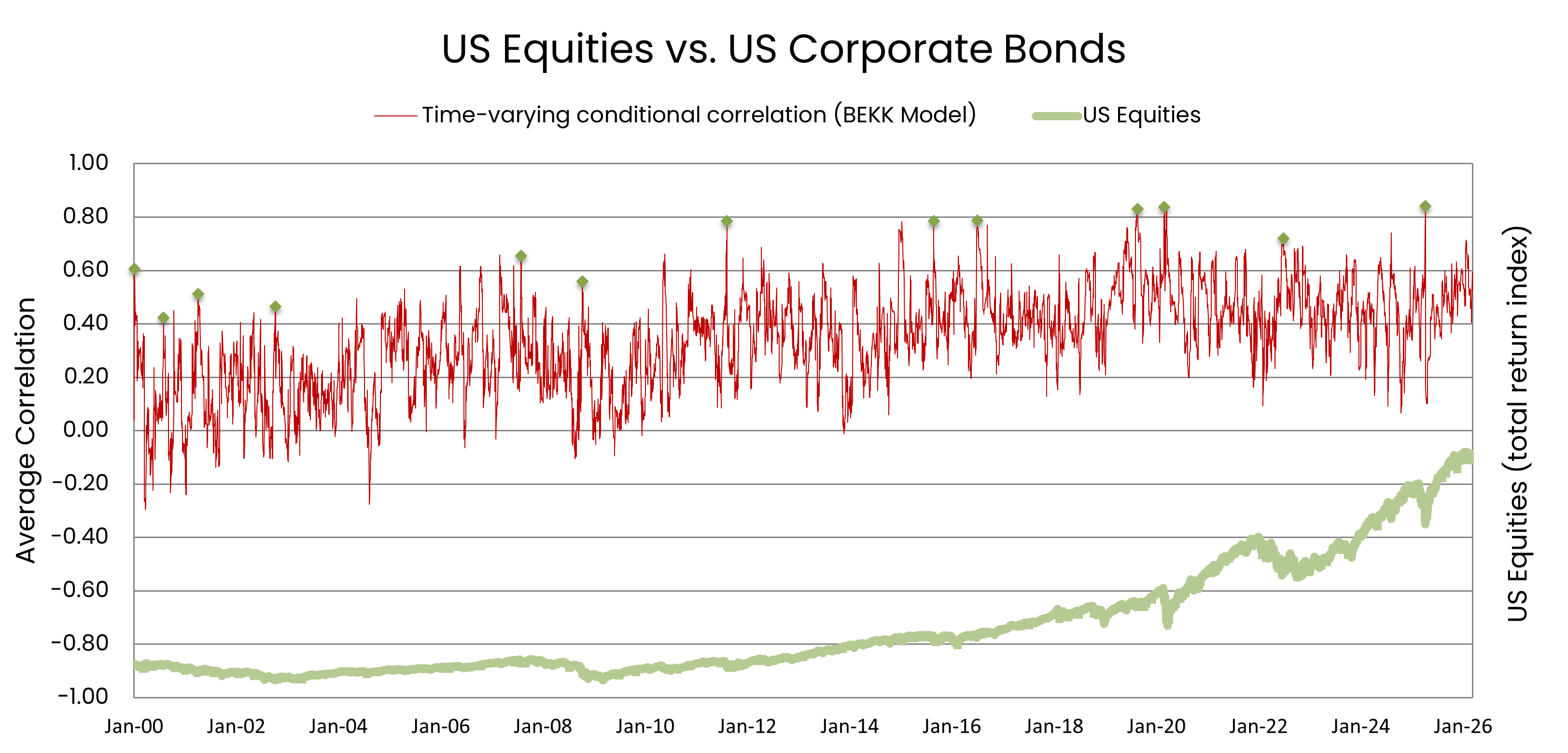

But unfortunately, reality looks different. Correlations are dynamic and oscillate dramatically over time. A look at the historical correlation between US equities and US corporate bonds (in USD) makes this advice error clear:

As you can see, the lockstep between these two supposedly different assets is anything but constant. In quiet times, the correlation may be low, supporting diversification theory. But whenever things get really dicey on the stock markets – for example during the dot-com crash, the financial crisis, or the COVID pandemic – the correlation shoots up. In crash phases, it almost always approaches the 0.6 to 0.8 mark. Exactly when you need the diversification effect most, everyone suddenly starts performing the same synchronized dance downwards.

The Fair-Weather Umbrella: Why Standard Advice Fails in a Crisis

You can think of this type of diversification as a fair-weather umbrella. It works perfectly as long as the sun is shining or there's just a light drizzle, providing a deceptive sense of security. But the second a real storm breaks out, the umbrella simply folds up.

This is due to a mechanical and psychological phenomenon: the liquidity effect. In crises, investors come under pressure (e.g., through margin calls or panic). They urgently need to obtain liquidity. In that moment, they don't sell what they want to sell, but what they can sell – everything that is liquid.

'The only thing that rises in a crisis is correlation.'

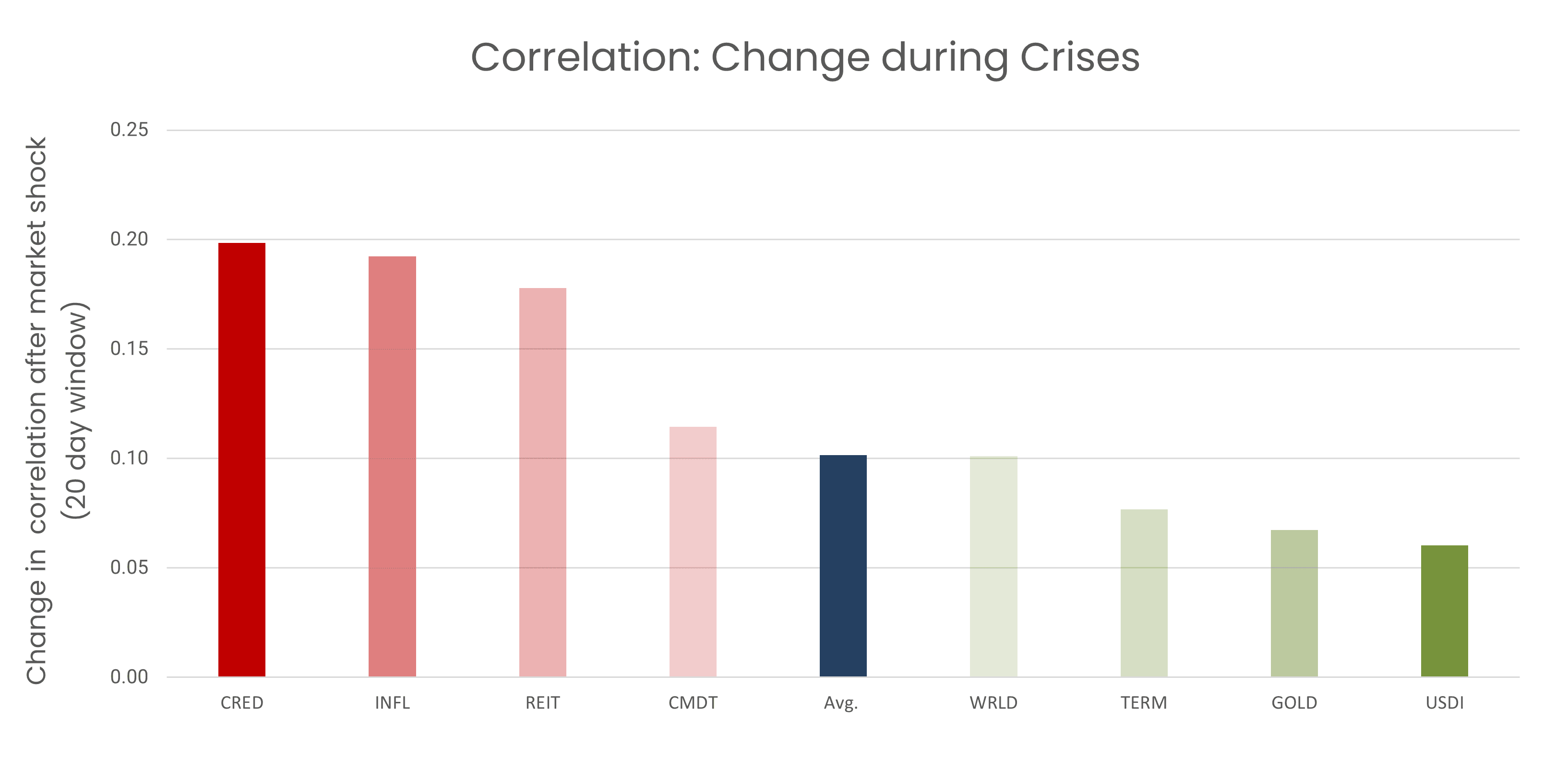

Suddenly, almost everything correlates towards 1. Against the systemic risk of the overall market, the diversification across countless asset classes often praised in advisory meetings is frequently powerless in times of need. The following analysis of the change in correlation in the first 20 days after a market shock proves this effect empirically:

The picture is clear: no matter how 'risk-free' an asset is considered compared to stocks in theory (such as US government bonds/US Treasuries), the correlation always increases dramatically after a crisis. This universal lockstep is direct proof of the liquidity effect: the flight to cash forces investors to dump all asset classes at the same time, which pulverizes the theoretical diversification benefits.

When the Buffet is Free, but the Waiter is Unaffordable

When the 'free lunch' is served in an advisory meeting, the fine print often falls under the table. Jennings & Payne showed the bitter truth in their 2016 paper 'Fees Eat Diversification’s Lunch': the buffet may be free, but the waiter is extremely expensive.

Every additional complex product added to a portfolio brings marginal costs. There is a tipping point where the costs of additional diversification exceed the theoretical benefit of risk reduction. We call this 'di-worse-ification'. When portfolios with assets of less than CHF 100,000 contain more than 20 different products, it is no longer thoughtful risk management – it is the result of wrong advice and a pure fee machine that eats up investment success.

The Real Crisis Currency: Cash and the Goal-Based Way

If diversification across more and more asset categories (inter-asset) fails in a crisis and only costs fees – how do you really prepare yourself? The mathematically most honest answer is: Cash and the money market.

Instead of managing risk through poorly advised, shaky portfolio structures and expensive additional assets, we at goal-based.investments use the concept of the tangential portfolio. This means: a highly efficient, worldwide stock engine is built for returns. Risk management, however, does not happen by adding expensive exotics, but through the most uncorrelated asset in the world: cash.

To protect against di-worse-ification and classic advice errors, we take a consistent path as a robo-advisor:

1. Complexity grows with assets: To ensure that even small wallets are not eaten up by minimum fees, at goal-based.investments the number of recommended ETFs increases proportionally with the investment assets. The portfolio receives exactly the structure that is efficient for the respective amount – no more and no less.

2. The real crisis brake: We are the only robo-advisor in Switzerland that standardly includes a cash allocation up to a portfolio with an 80% equity share. When the market crashes and correlations jump to 1, cash is the only umbrella that remains reliably open. This is the only way to truly manage risk precisely in an emergency.

Conclusion for the Goal Portfolio

Diversification is not a magic shield, but a tool that must be used with surgical precision. Those who invest cleverly do not allow themselves to be dazzled by pseudo-complex advice myths.

• Question costs: Does the 20th fund in the portfolio really bring more security or does it just feed the 'waiter'?

• Intelligent scaling: Broad diversification within an asset class (intra-asset), but keep the number of products appropriate for your own assets.

• Cash is King (in risk management): Real risk is not managed through an expensive obsession with collecting products, but through a solid cash allocation.

At goal-based.investments, we believe: True security does not come through maximum complexity, but through the clarity that investments fit your personal goals – calm, cost-efficient, and crisis-resistant.

And if you want to expand your investment know-how beyond diversification, you are cordially invited to do so in our Do-It-Yourself training courses. Just one click is enough!